What Should I Think Now? Responding to COVID-19 and the CARES Act.

How does Coronavirus and the CARES Act affect your business? What should you be thinking? See our latest thinking here.

VALUATIONS IN HISTORICAL CONTEXT

Prior to the Coronavirus epidemic, the S&P 500 (blue line) was trading 123% above the 160-year regressed mean (red line). Even after recent market volatility, the market is still trading 86% above the mean. So, public valuations remain high relative to historical performance.

Does The Cares Act create a dilemma with low-wage earners?

Though information about the CARES Act seems to be rapidly evolving, and, in some sense, changing by the hour, a potential wage dilemma could arise that could cause headaches for some employers. The issue lies in the fact that low wage earners could receive considerably more income by taking unemployment benefits than they could by earning normal wages in their job or by rejoining the employer that was forced to let them go.

In the majority of states, maximum unemployment benefits range from $300 - $500 per week. The CARES Act adds an additional $600 per week to this amount. An individual who lives in a state like North Carolina that pays a conservative $350 in unemployment benefits will now receive $950 per week. A state like Massachusetts, with a more generous $823 weekly unemployment benefit, could pay out $1,423 per week to the unemployed.

Now consider an employee in either of those states who earns $15/hour at their job: $15/hour * 8 hours * 5 days = $600 weekly earnings. It is clear that one could optimize their income potential by choosing unemployment over working a $15/hour job. In fact, in order to come out ahead of what one would make receiving unemployment benefits, a worker in North Carolina would need to earn over $23.75 per hour and a worker in Massachusetts would need to earn over $35.57 per hour.

Employers should consider the distortions that increased unemployment benefits might cause to their ability to retain workers or rehire workers, even as cheap or free money is made available for the express purpose of retaining those employees. In addition, unemployment taxes, which can range from 0.5% to over 10% depending on state and industry, should also be factored in as employers work through staffing situations.

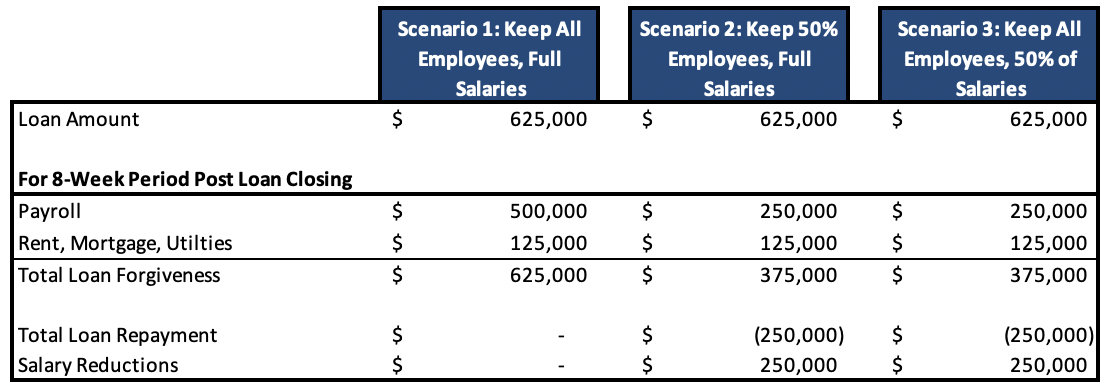

Notwithstanding the potential difficulty in retaining employees, the CARES Act does provide excellent terms for borrowing money. The loan scenario to the right describes a company with a $3M payroll, and below are three scenarios around retaining vs. laying off employees. Loans require no guarantee, no collateral, and all amounts used for payroll, rent, utilities, and interest on mortgage obligations incurred prior to February 15th will be forgiven.

Even companies who do not need a loan to retain or re-hire employees may want to consider applying for funding as the terms and cost of this capital are very attractive.

what are payment-in-kind (pik) loans

This is a non-recourse, no personal guaranty loan tailored to your company’s specific situation. It typically has no payments due within the first one or two years and is repaid within 7 to 8 years allowing the lender to participate in the future upside of the company, but without ever having to sell any stock ownership and it’s based on the future value of your company not the current value.

Perpetuate Capital endeavors to arrange these loans between Christian Family Offices and C12 members, as lenders, and C12 companies as borrowers throughout this year.

state of capital markets survey

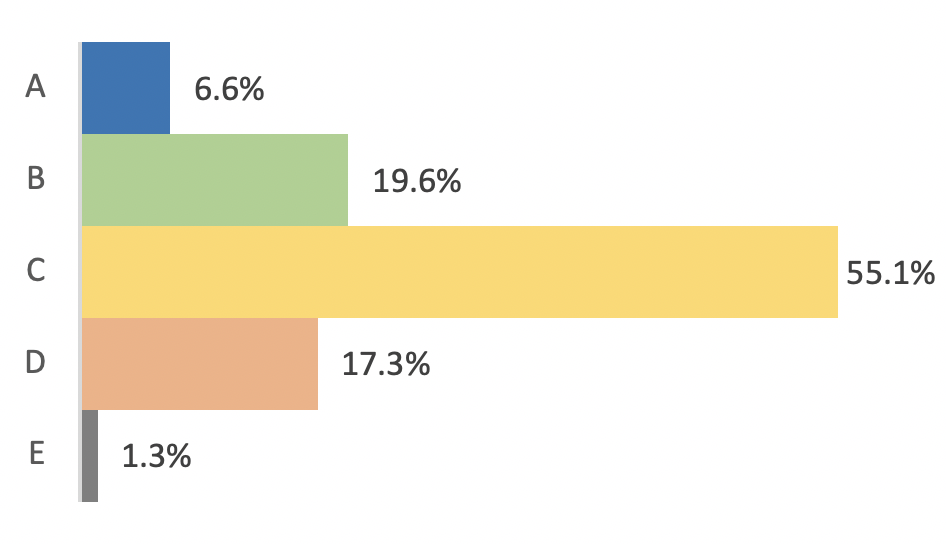

Perpetuate Capital, in partnership with PrivateEquityInfo.com, surveyed over 300 capital markets professionals across the country to get their sentiments on the current state of US financial markets. Below are the results of the survey, completed April 1, 2020.

How has your deal flow pipeline changed in March?

A. Significantly fewer opportunities

B. Moderately fewer opportunities

C. No change

D. Moderately more opportunities

E. Significantly more opportunities

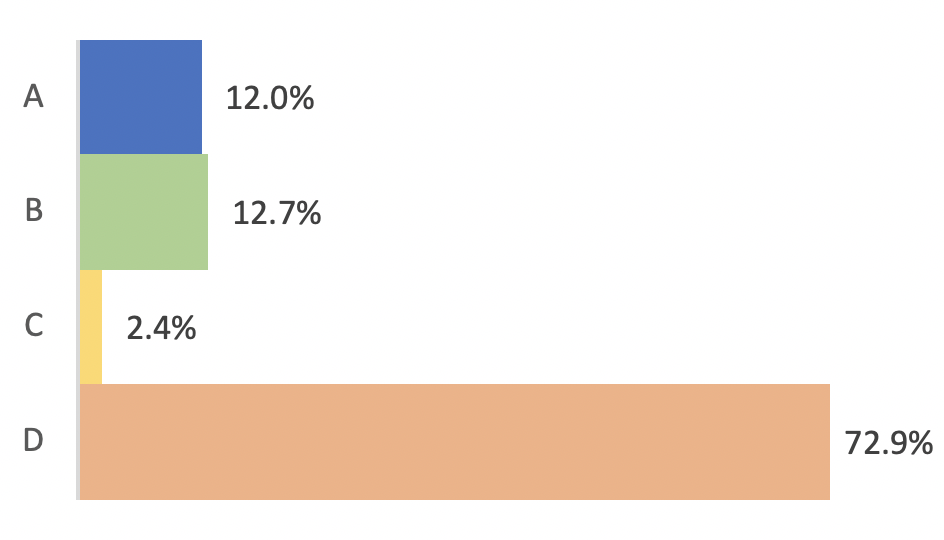

2. Did your February and March Deals close as expected?

A. No, all transactions cancelled

B. No, on hold until the dust settles

C. Some, not all

D. Yes

3. For deals closing, how are lenders reacting?

A. Higher rates plus more equity

B. More equity required

C. Higher rates

D. No change to terms

4. When do you think private company financial projections will be reliable again?

A. 3 months or less

B. 3 - 6 months

C. 6 - 12 months

D. Over 12 months

5. How do you expect private company valuations to adjust from the current economic shock?

A. No change

B. Down 0 - 10%

C. Down 10 - 25%

D. Down 25 - 50%

E. Down more than 50%

6. How has private equity investment appetite changed?

A. Unchanged from Jan & Feb

B. Unlikely to acquire in Q2

C. Unlikely to acquire in 2020

D. Wait-and-see mode

7. How are lenders behaving with respect to existing credits?

A. No change

B. Forbear on broken covenants

C. Moving more credits to workout

D. Calling in lines of credit

8. How are mezzanine lenders behaving for new opportunities?

A. Deals closing, terms consistent with pre-Feb deals

B. Deals closing, changes to terms

C. Stalled, pending market conditions

Comments from survey respondents:

“Really tough to say for sure on these questions - too early. But lenders are tightening leverage finance pricing/terms. Everybody is wait-and-see. PE is holding back "dry powder" to provide cash to existing portfolio companies. Hoping existing lenders will step up, but concern that credit won't be available even for long-term, good borrowers.”

“Answers to these questions vary widely depending on the industry. Some are up, some are down, some are unchanged. Also varies by size of the deal and whether or not the buyer is a strategic.”

“Funds aren't going to close any deals until things settle down, if for no other reason than LPs would think they were nuts to do so.”

“More opportunities in the market are likely to appear post COVID-19 (in 3 months) but market likely to exercise more caution.”

“More opportunities for special opportunity M&A. High quality targets are more receptive for proposals.”

“No big changes yet. One deal, with fracking exposure is suspended. Others who are enhanced by this environment are moving nicely to close.”

“Not losing deals but many are being deferred and will wait until the pandemic has subsided.”

“Business success and valuations will be largely linked to the sector in which they operate.”

“90% of our current transactions are moving forward as planned, some have supply chain issues.”

“Buyer activity has virtually dried up. Sellers are now nervous as their business value decreases.”

Perpetuate Capital White Paper

Approximately 2,000 private businesses in the United States are currently owned by committed Christians who provide varying levels of support for domestic and international ministry and missions

Approximately 2,000 private businesses in the United States are currently owned by committed Christians who provide varying levels of support for domestic and international ministry and missions within and outside the company. Because most of these business owners believe God is the actual owner and that they are merely stewards, the title of Businesses as a Ministry (BaaM) has been adopted to characterize them. The profits of these companies fuel giving to the Kingdom both directly and through owner tithing to local churches and mission budgets. BaaM owners are stewards that view the operation, culture and rich ministry within and through the business as something to be preserved.

The owners of BaaMs face unique financial difficulties as they manage their business because of the importance of maintaining owner control in order to continue ministry support both during and after their involvement in the business. The provision of shareholder liquidity and funding the retirement of owners is complicated by the difficulty in obtaining capital from traditional sources because of a portion of profits being diverted to ministry support both inside and outside of the company. BaaMs require access to a type of capital that does not require them to give up control of their business.

Private Equity Acquisition Trend

Of the approximately 100,000 companies in America that employ at least 100 employees, it is estimated that an average of 4,000 of these companies have been acquired each year by private equity firms since the early 1990s. It is reasonable to infer from these numbers that 30% to 40% of private companies with at least 100 employees are now owned by secular private equity firms focused exclusively on profit. This trend will continue for demographic reasons as Baby Boomer private business owners reach retirement age.

Owners of private businesses who want to liquidate all or a part-interest in their company typically sell to a private equity firm. This prevalent practice is a consequence of one of two unfortunate situations. The first is that the typical owner and management team are not aware of any alternative means of obtaining significant liquidity while maintaining control of the company. The second is most of the outside financial and legal advisors providing guidance to management are typically not familiar with any alternative to a business sale to a third party private equity firm or strategic, industry buyer.

Liquidity Options for Business Owners

When a business that allocates a portion of profits to ministry support (BaaM) is acquired by a private equity firm or industry buyer, the diversion of a portion of profit to ministry support will be immediately terminated as will any ministry occurring for employees within the organization.

There is an urgent need for private business owners to be made aware of an alternative to the prevalent practice of selling a business to private equity firms or industry buyers in order to obtain the liquidity necessary to fund the retirement of owners. This alternative liquidity option would provide the following advantages:

Fund the retirement / major liquidity distributions for owners

Enable continuation / succession of owner control of the company

Permit the diversion of significant profit for charitable purposes

Facilitate beneficial employee stock ownership without cost to employee

Enable permanent reduction or elimination of corporate level taxes

In addition to the above benefits of such an alternative, significant personal tax advantages would be available to cover costs of implementing and taking advantage of such an alternative.

Inception of the Employment Stock Ownership Plan

The employee stock ownership plan (ESOP), also alternatively known as the employee share ownership trust (ESOT), was conceived in 1956 by Louis Kelso, a San Francisco attorney and investment banker. A book written by Louis Kelso and the author and philosopher Mortimer Adler, and published in 1958, “The Capitalist Manifesto”, explained the macro-economic theory upon which the ESOP initiative was based.

The thesis of the book is that democracy is the only method of government worthy for human beings and that Capitalism is the only system that can sustain democracy, because only in the possession of the means of production can a person be truly free. The authors also wrote (over 60 years ago!) that we faced a real and present danger from the progressive socialization of our economy. They recommended that tax policy should be implemented to encourage beneficial ownership of stock by employees to supplement their income and preserve our capitalist system.

As a consequence of the work by Louis Kelso for nearly two decades, his proposals were finally incorporated into a major reform of retirement law known as ERISA (Employee Retirement Income Security Act of 1974). Among the beneficial provisions are the following:

ESOP-owned companies receive tax deductions for payments to employees

Employees receive beneficial stock ownership at no cost

ESOP trusts could borrow money to buy company stock

Loans can be repaid out of tax-deductible corporate contributions

Deferral or elimination of capital gains for certain sellers of stock to ESOP

National Center for Employee Ownership (NCEO)

This private, non-profit, membership, information and research organization was founded in 1981, by Corey Rosen, who had worked as a professional staffer in the U.S. Senate, where he helped draft ESOP legislation. The purpose of the organization is to educate business owners on employee stock ownership and managers of ESOP owned companies on measurement and improvement of their ownership cultures. NCEO also produces publications and ESOP sample documents for the benefit of their membership.

The ESOP Playbook

This book was written and published in 2017, by Brandt Brereton, the author of this post, and Jared Hanley, the two principals of Brereton Hanley, a boutique investment bank in Silicon Valley. Their objective was to utilize their extensive experience, in advising companies for more than two decades regarding ESOPs, to accomplish two purposes with the book. The first was to explain what an ESOP is and how a typical sale to an ESOP is conducted. The second was to provide an introduction to the many tools and alternatives that an ESOP can provide to a business. Because business owners can sell even 100% of their shares and still retain control of the company indefinitely, the author’s hope is that this expertise can be taught and focused on the attrition of BaaMs problem.

A unique and very helpful feature of the book is the comparative analysis of the three most common corporate finance transactions: (1) the M&A (industry buyer) sale, (2) the Private Equity sale, and (3) the ESOP sale. For each type of transaction, the process is described, the parties and their agendas are discussed, and the pros and cons of the respective finance transaction types are enumerated. The parties covered for each transaction type are sellers, buyers, attorneys, CPAs, investment bankers and employees.

Emergence of Perpetuate Capital

Brereton and Hanley joined a team of Christian entrepreneurs recently to form Perpetuate Capital, an investment fund organization to provide a market-based source of capital to Christian owned businesses without detrimentally impacting their culture, independent control, legacy and ministry. Investor returns are targeted at or above historical, secular market averages, which can be achieved by the right professionals.

Among the uses of the capital could be the purchase of shares held by a departing owner in a private company by using an ESOP, funding traditional management led buyouts without the use of an ESOP, aiding in the divesting and acquiring of subsidiaries, and providing growth capital to profitable businesses. Perpetuate Capital exists to perpetuate the Kingdom impacts of BaaMs, while solving for shareholder liquidity at market-based costs/returns with fully aligned investors.

The key component of the initiative is the establishment of a structured equity fund that will accept investments of any denomination only from Christian individuals and entities and only provide that capital to BaaMs. The objective of the fund is to provide a return in the ballpark of 12%, which is the average return for secular structured equity funds over the last 25 years. Additional information about Perpetuate Capital and our partners can be found on our website at www.perpetuatecapital.com. In addition to contact information, the website provides the following categories of information:

We feel privileged to dedicate our God-given experience sets and what remains of our earthly sojourns to focusing on this achievable solution to a very tragic but avoidable problem. We are optimistic that the Kingdom giving of existing BaaMs can not only be preserved but increased. Also, we are hopeful that additional Christian owned businesses can be transitioned to BaaMs with this new knowledge and capital provision.